U.S. Green Transition: Strong Sector Momentum in 2026

Recent news coverage may give the impression that the green transition is facing considerable challenges, with shifting federal priorities and reports of policy uncertainty raising concerns about whether progress is slowing.

Even so, the underlying indicators in this article point to continued movement across the U.S. energy system. The discussion that follows focuses on where momentum is showing up in practice, from the states and regions adding new capacity to the fast-growing electricity needs of data centers, and from the buildout of charging to the growing role of new capacity, efficiency, and storage.

The One Big Beautiful Bill Act (OBBBA) signed in July 2025 introduced new regulatory measures aimed at addressing national security and foreign influence concerns. As a result, the bill imposed stricter trade and procurement rules that affect clean energy infrastructure. While these changes may present challenges for renewable energy development, they have also prompted a notable increase in activity as developers work to adapt to the evolving landscape, highlighting the growing importance of renewable energy within the U.S. grid and economy.

The 2026 Energy Outlook

As policy headwinds dominate the headlines, there is still ongoing momentum. While federal funding decreased for wind and solar programs in FY2026, funding increased for geothermal, hydropower and grid technologies.

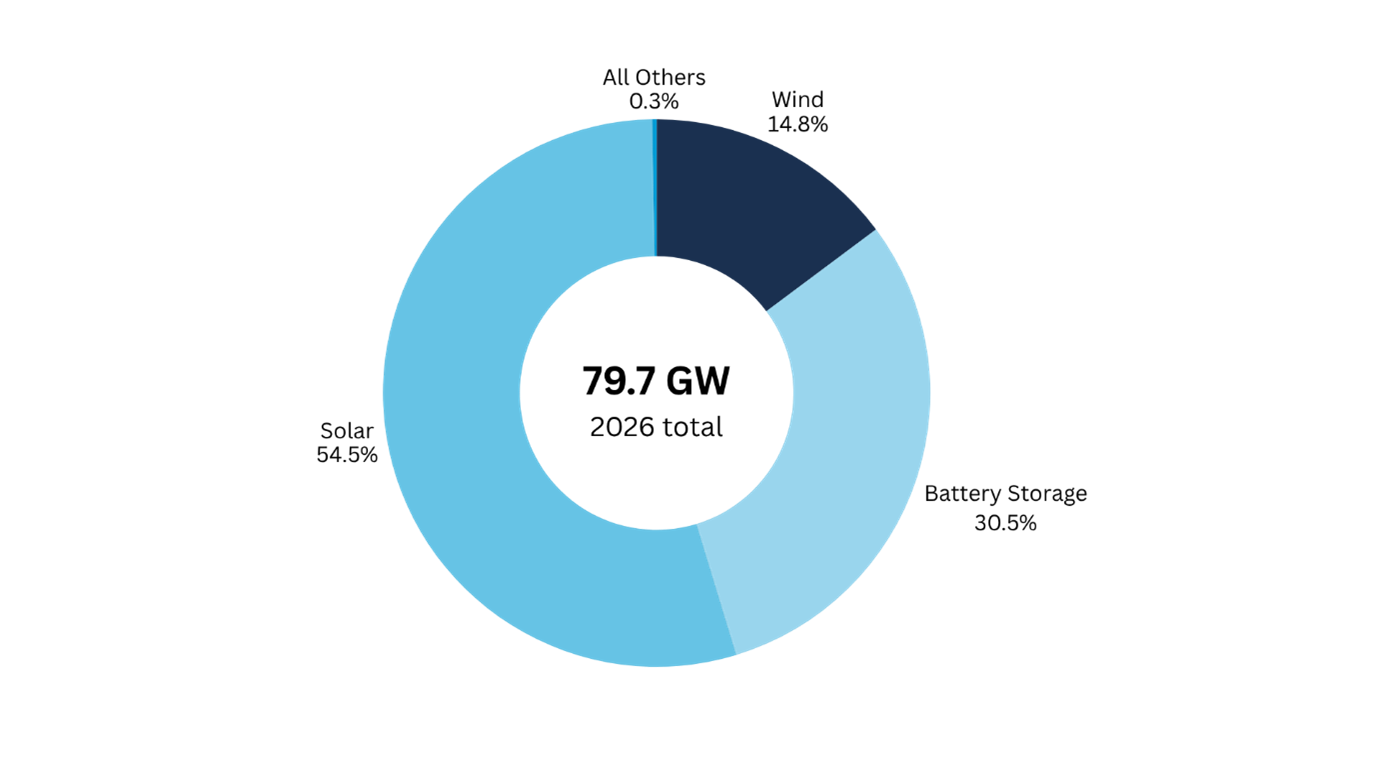

According to the U.S. Energy Information Administration (EIA), developers plan to add more than 79.7 gigawatts (GW) of utility-scale solar, battery, and wind due to the high demand. 79.7 GW can power roughly 15 million average American homes annually. Leading the way in the deployment for 2026 are states such as Texas and California, both of which are accelerating their clean energy initiatives and are set to add significant new utility-scale solar capacity in response to growing demand and favourable state policies.

This surge in planned capacity is not occurring in isolation, but is being shaped by evolving federal regulations and incentives, which are rapidly influencing the actions of developers across the country.

Due to the OBBBA, the U.S. Internal Revenue Service (IRS) issued a notice for developers to lock in the higher, previous-year’s tax credit rates by proving that “construction has begun” before deadlines are revised. Developers are now racing to take advantage of safe-harbor provisions before new federal sourcing and tax-credit rules fully take effect. These changes are accelerating the timeline for renewable projects that wish to claim the solar investment tax credit (ITC).

As a result of the pressures created by the new Foreign Entity of Concern (FEOC) rules, which restrict components being sourced from certain countries, developers must diversify where they get solar panels, batteries, and critical minerals to avoid disruptions or credit losses. This diversification allows for an expansion of the renewable-energy sector as it reduces vulnerability and enables more stable growth even under policy or supply-chain pressure. This is, however, not without its challenges. The FEOC rules, which restrict sourcing components from countries such as China, a major supplier of solar panels and critical minerals, creates significant obstacles for developers. While the need to diversify sourcing may reduce vulnerability and attract investment in the long run, the immediate effect of FEOC regulations complicates supply chains and potentially slows sector growth.

There is also surging demand for electricity, especially as data centers continue to expand rapidly across the United States.

The Data Center Revolution

Amid the AI boom, data centers are emerging as one of this decade’s most critical resources. According to the U.S. Department of Energy, the data center annual electricity use in 2023 was approximately 176 terawatt-hours (TWh), approximately 4.4% of U.S. annual electricity consumption. However, projections show that data center electricity consumption could double or triple by 2028. For reference, Sweden’s total electricity production was 169 TWh in 2024.

It is estimated that more than 50% of the electric power demand of data centers stems directly from the operation of electronic IT equipment. The rest is used for cooling, dissipating heat to maintain optimal performance and overall system stability and accounts for 38% to 40% of electricity consumption in a data center.

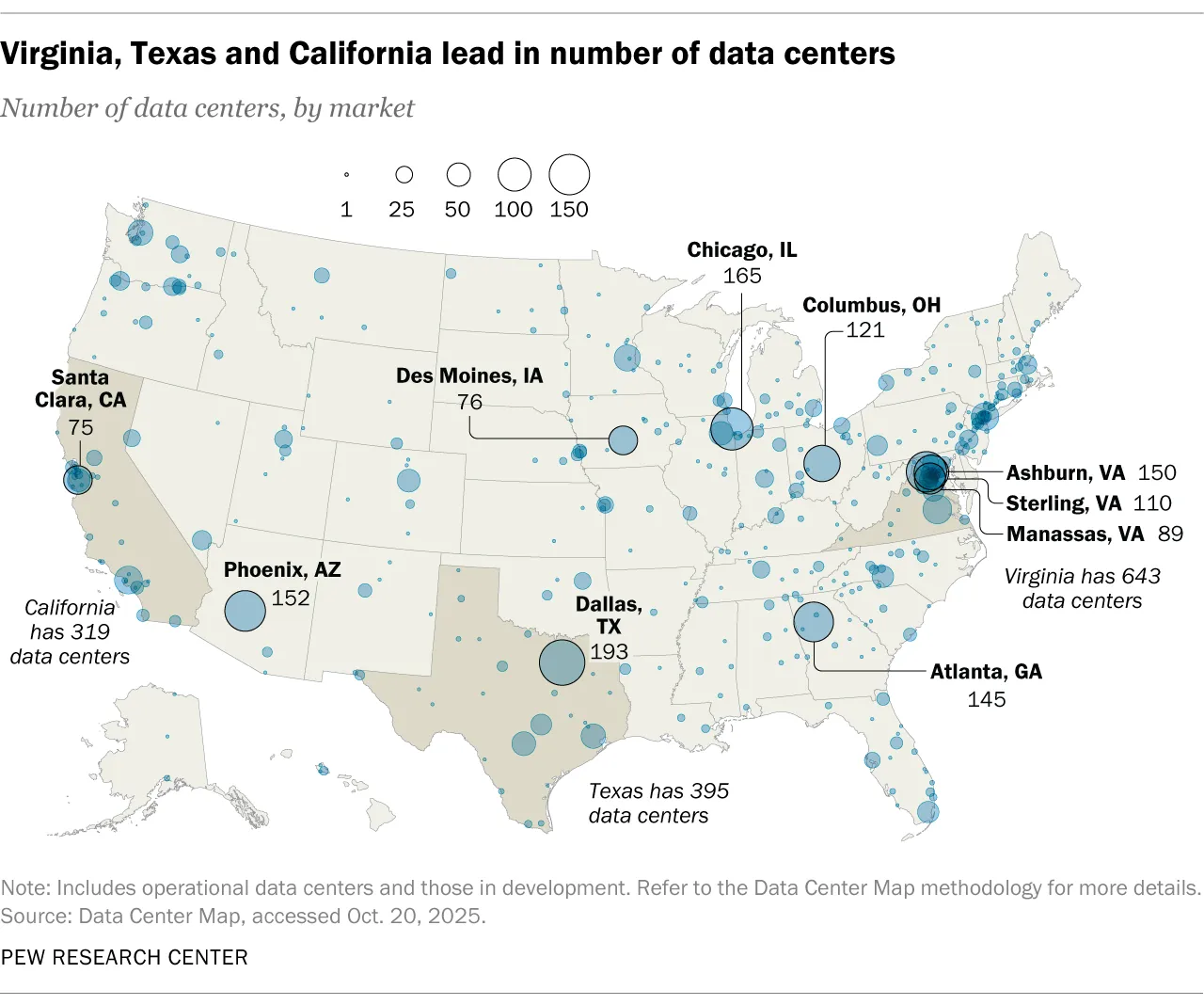

The U.S. has over 4,000 data centers, including operational sites and those under development. A third of U.S. data centers are in just three states: Virginia (643), Texas (395), and California (319). These states are well positioned for future projects due to proximity to customers and their favourable cost considerations involving land, construction electricity prices, and state incentives.

Renewable Energy Within Data Centers

As of 2024, natural gas supplied over 40% of electricity for U.S. data centers. Renewables such as wind and solar supplied about 24% of electricity. Progress is being made already with several key data centers run entirely on renewable energy. A notable example is the Eagle Mountain Data Center. Operated by Meta, it is one of the world’s largest single-site data centers with more than 900,000 square feet and scalable multi-hundred-MW IT capacity.

However, due to increasing electricity demand from data centers, there is a steep increase in energy constraints regionally. Industry disclosures suggest that by the end of the decade, a meaningful share of new data center capacity could be partially or fully self-supplied. As concerns about energy access and prices are being voiced, states including California, New Jersey, and Virginia have weighed bills requiring or incentivizing data centers to draw some of their power from renewable energy sources.

What States are Stepping Forward?

As of early 2026, 35 states have enacted Renewable Portfolio Standards (RPS) or Clean Energy Standards. In light of the OBBBA, states are accelerating their clean energy initiatives, specifically California and Texas. California’s Governor Gavin Newsom signed an executive order in 2025 to protect the state’s progress and double down on building clean energy faster. The executive order designates the Energy Working Group of the Governor’s Infrastructure Strike Team to track projects eligible for tax credits and requires state agencies’ actions to accelerate clean energy project development. It also enables relevant state agencies to prioritize projects beginning construction before the OBBBA’s revised deadlines.

The state of Texas is also accelerating their renewable energy initiatives. Texas added roughly as much utility-scale solar capacity in 2025 as it did in 2024. Now, it has one of the largest, utility-scale solar generation capacity in the country. Even with rising tariffs and reduced federal incentives, solar remains one of the fastest and most deployable sources of new capacity available to the state.

Texas and California, among others provide concrete examples of the accelerating momentum in the country for a continued shift towards renewables. Despite Federal pushbacks, states retain the autonomy and determination to sustain and build upon the momentum established in previous years. State-level leadership, policy innovation, and local economic incentives continue to drive investments and progress in renewable energy, ensuring that the clean energy transition remains firmly underway.

Electrifying Mobility

The transition sustainable mobility has moved well beyond the initial phase of passenger electric vehicle (EV) adoption, which reached nearly 1.6 million units sold in the U.S. in 2025, capturing approximately 8% of all domestic new car sales, evolving into a highly interconnected, software-defined ecosystem. The U.S. market for Software-Defined Vehicles (SDVs) is now valued at over $109 billion and is projected to grow at a compound annual growth rate (CAGR) of over 32% through the next decade. Today, the focus has shifted from merely replacing internal combustion engines to deploying holistic, data-driven mobility networks. This next phase is characterized by the acceleration of heavy-duty commercial electrification, where over 12% of new Class 7 and 8 trucks sold in the U.S. are now electric, marking a fivefold increase since 2022. Furthermore, it is driven by the integration of autonomous fleet technologies, with autonomous vehicles surpassing 145 million miles driven on U.S. public roads by 2025 and the convergence of domestic transportation networks with decentralized energy grids. Advanced artificial intelligence is optimizing this Vehicle-to-Grid (V2G) energy exchange, a U.S. market expected to exceed $24.5 billion by 2035 as EVs are transformed into dynamic virtual power plants.

Evidently, the United States has made substantial progress in supporting the growth of EVs by installing over 300,000 public charging ports across the country including a landmark surge past 70,000 high-speed DC fast-charging stalls in early 2026. These efforts are part of a broader strategy to make EV adoption feasible for a greater number of Americans, with charging infrastructure now spanning urban centers, highways, and rural areas. However, the current trend is pivoting from sheer geographical expansion toward high-performance, purpose-built infrastructure. A major focal point is the rapid deployment of Megawatt Charging Systems (MCS) designed to support long-haul electric trucking and logistics fleets across interstate corridors. As range anxiety subsides for everyday consumers, both public and private stakeholders are actively prioritizing smart depots and AI-optimized routing that minimize charging downtime and maximize fleet operational efficiency.

Buildings Solar Adoption and Energy Efficiency

The rapid adoption of solar panels across commercial buildings has become a defining trend in the push for energy efficiency and sustainability. Over the past few years, there has been a 45% surge in on-site renewable installations in commercial properties, driven by a combination of tax credits, grants, and state-mandated requirements. 60% of commercial properties are now equipped with solar installations, and businesses are seeing a significant reduction in their reliance on traditional energy sources, amounting to a 25% decrease. The visible integration of photovoltaic arrays on office complexes, shopping centers, and warehouses highlights a new standard for urban and suburban development where clean energy generation is both a practical and economic choice.

These financial and policy tools have made it increasingly appealing for property owners and developers to invest in solar as well as energy efficiency and energy storage technologies, often offsetting initial installation costs and providing long-term fiscal benefits.

Energy storage is becoming increasingly important for commercial buildings as they transition to renewable energy sources like solar. By integrating storage solutions, businesses can maximize the use of on-site solar power, ensuring that energy generated during peak sunlight hours is available around the clock. This not only helps offset utility costs and lowers reliance on traditional power sources, but also enables commercial properties to manage energy demand more efficiently, avoid peak pricing, and support grid stability. With energy storage, buildings can maintain uninterrupted operations, reduce curtailment of solar generation, and achieve higher levels of energy independence and sustainability.

Alongside on-site generation, much of the near-term opportunity in U.S. buildings is coming from energy efficiency and smarter operations. Building owners are increasingly investing in digital tools for energy optimization, such as Building Energy Management Systems (BEMS) and advanced controls that monitor performance in real time and reduce waste without major structural changes. Upgrades to high-efficiency equipment, especially HVAC systems, are also gaining momentum, as are improvements to building envelopes through better materials and insulation that cut heating and cooling demand at the source. This shift is being reinforced by city- and state-level building performance standards that are tightening expectations for large buildings in markets such as New York, California, Washington, and Washington, DC, creating steady demand for proven efficiency solutions and services.

As the U.S. continues to advance its renewable energy efforts across sectors, the next phase requires coordinated strategies and partnerships to maximize impact and drive sustainable growth.

Where GTI Comes In

Amidst the changes, Green Transition Initiative provides a platform for U.S. and Swedish stakeholders to collaborate and build on this momentum. It is imperative that we take advantage of this propulsion. While it may seem that Federal regulations are slowing the progress of renewable energy initiatives in the U.S., the reality is that numerous regions are forging ahead with ambitious expansion.

Some of our current work includes coordinating a letter of intent between Sweden and California on green transition we recently hosted a delegation to Dallas in order to highlight opportunities for Swedish companies.

We are also preparing to launch a new program focusing on energy efficiency in data centers, targeting key regions such as Virginia, Texas, and California. These upcoming initiatives will create valuable opportunities for collaboration and innovation in sustainable technology.

This is where GTI comes in. By fostering international collaboration, providing guidance, and connecting key stakeholders, we help accelerate the deployment of energy efficient technologies and facilitate the transition towards cleaner, more resilient energy systems. Together, we can turn today’s momentum into enduring progress for a sustainable future.

If you are interested in working with us, find contact details here.